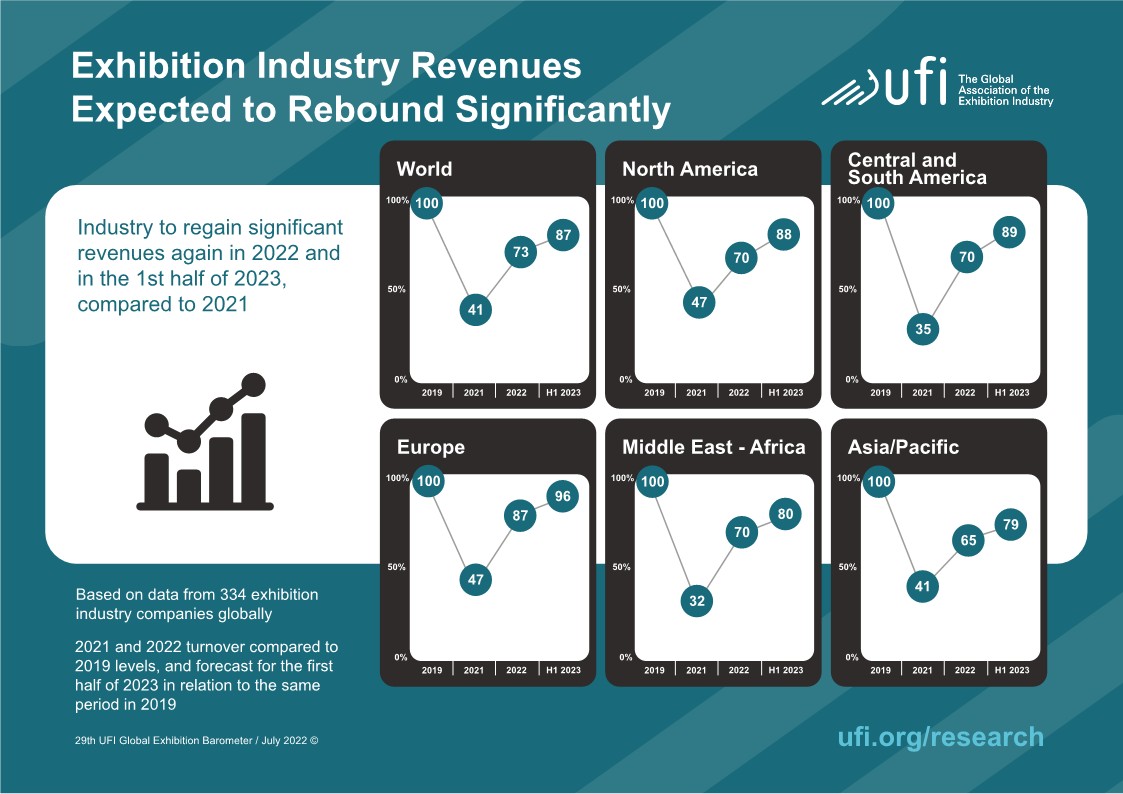

– Global exhibition revenues are expected to reach 73% of pre-pandemic levels in 2022, and 87% in the first half of 2023

– 70% of companies expect to be operating at normal levels from September 2022

– Management challenges (such as staffing) and digitisation are the most pressing industry issues, with 69% of companies currently undergoing recruitment drives

– The complete Barometer report includes dedicated profiles for 28 markets and regions

Paris – 26 July: UFI, the Global Association of the Exhibition Industry, has released the latest edition of its flagship Global Exhibition Barometer research, which takes the pulse of the industry.

The results highlight the quickening pace of the industry’s recovery in 2022, after the continuing impact of COVID-19 throughout 2021. The sector is bouncing back quickly, and revenues for the first half of 2023 are expected to reach 87% of comparable 2019 levels (noting that 2019 has been the industry’s record year to date).

In terms of operations, around six in ten companies are reporting “normal activity” – up from just three in ten, six months ago. By the end of the year, seven in ten companies expect to be operating at normal levels, while only around 5% of companies still expect to have “no activity” from September 2022.

When asked what elements are most crucial to supporting the “bounce-back” of exhibitions, six in ten companies selected “Lifting of current travel restrictions” and “Readiness of exhibiting companies and visitors to participate again”. The two next most influential drivers are “Financial incentive packages (leading to reduced costs for the exhibitors)” and “Lifting of current public policies that apply locally to exhibitions”, mentioned by four in ten and three in ten companies respectively.

In terms of 2022 operating profits, 25% of companies globally are expecting either a loss, or a reduction of more than 50%, compared to 2019 levels. Overall, 73% of companies received no public financial support during the pandemic, and for the majority of those that did, financial public aid represented less than 10% of their overall costs.

The most pressing business issues reflect how the industry is now focusing on post-pandemic challenges and opportunities. “Internal management challenges” (highlighted by 20% of respondents), “Impact of digitisation” (17%) and “Competition with other media” (15%) are the most common. Meanwhile, the “Impact of the COVID-19 pandemic on the business” has dropped from being the most pressing business issue to the sixth-most pressing issue (a drop from 19% to 11%), compared to the previous edition of the Barometer.

“The bounce-back of exhibitions around the world has entered its next phase, and pre-COVID levels will be within reach as early as next year in some markets,” says Kai Hattendorf, Managing Director and CEO at UFI. “As the industry manages this amazing recovery, it is also dealing with significant staffing challenges, and is working to apply key learning from the pandemic around the digitisation of events and services into its business model.”

Size and scope

This latest edition of UFI’s bi-annual industry survey was concluded in June 2022, and includes data from 366 companies in 57 countries and regions.

The study also includes outlooks and analysis for 23 focus countries and regions – Argentina, Australia, Brazil, Chile, China, Colombia, Germany, Hong Kong, India, Italy, Japan, Malaysia, Mexico, Saudi Arabia, Singapore, South Africa, South Korea, Spain, Thailand, Turkey, the UAE, the UK and the US – as well as five additional aggregated regional zones.

Operations: reopening exhibitions

Spain, Turkey and the UK, in Europe, Saudi Arabia and the UAE, in the Middle East, and Australia and Brazil stand out as markets where the majority of companies returned to normal activity levels in early 2022. Globally, the majority of markets reached this point in March 2022. Notably, Asia, as a region, only reached this point in May (with China not expecting to reach this point until October, and for Hong Kong not until next year).

Turnover, operating profits and public financial support

Globally, and on average, companies have seen a significant increase in their 2022 turnover, which now represents 73% of 2019 levels. They also project this to increase to 87%, using the same baseline for the first half of 2023.

Many countries are performing well above average. In particular:

– for 2022 revenues, the UK (89% of 2019 levels), Italy (86%), Saudi Arabia (85%), Turkey and South Korea (82%) and Japan (80%) Contrasting are the results from Hong Kong (34% of 2019 levels), China and South Africa (both at 57%) and Malaysia (59%)

– for projected revenues for the first half of 2023, most markets are expecting at least 75% of 2019 levels, with only Hong Kong (58%) China (69%) and South Africa (72%) expecting lower levels.

In terms of operating profit for 2022, 10% of companies globally are expecting a loss, and 15% are expecting a reduction of more than 50%, compared to 2019 levels.

Several regions include countries with a higher-than-average proportion of companies foreseeing a loss in 2022. In particular:

– Brazil (13%) in Central and South America

– Germany (15%) and Italy (13%) in Europe

– Australia (14%), China (21%), Hong Kong (20%), India (17%), Singapore (20%), South Korea (11%) and Thailand (40%) in Asia-Pacific.

In terms of public financial support, Asia-Pacific and Europe saw the highest proportions of businesses receiving such funding (37% and 35% respectively).

In all regions, there are significant differences across markets, as can be seen in the following percentage ranges of companies declaring they received “no public support”:

– from 10% in Hong-Kong to 92% in India, in Asia-Pacific

– from 38% in Germany to 86% in Turkey, in Europe

– from 58% in Colombia to 100% in Chile, in Central and South America

– from 69% in Saudi Arabia to 100% in the UAE, in the Middle East and Africa.

Digitisation

Overall, 65% of respondents have added digital services/products (such as apps, digital advertising and digital signage) to their existing exhibition offerings. This is especially the case in Asia-Pacific (71%).

In addition, while 49% of respondents globally indicated they have digitised internal processes and workflows, this number was higher in the Middle East and Africa (62%) and Europe (55%).

While 32% of respondents globally have developed a digital or transformation strategy for exhibitions and products, this number was higher in Central and South America (38%).

Staff recruitment

Globally, 69% of companies are currently in the process of recruiting more staff, with 62% facing difficulties with sourcing appropriate candidates.

In all regions, most companies are currently recruiting more staff, while at country level, China is the only country where a majority of companies are not recruiting.

Key business issues

“Internal management challenges” is the key business issue for all regions, and it is the most selected issue for most markets, with staffing being the most prevalent of these challenges.

Some differences can be seen in relation to “Impact of digitisation”, which is the most pressing issue in Colombia (24%) and Germany, Malaysia and Thailand (20%). Meanwhile, “Impact of the COVID-19 pandemic on the business” remains the most important business in China (21%) and Hong Kong and Japan (20%).

An analysis per industry segment (organiser, venue and service provider) shows no differences with regard to the three most important issues, which remain “Internal management challenges”, “Impact of digitisation” and “Competition with other media”.

Future exhibition formats: physical and digital events

In addition to the 87% of companies who are confident that “COVID-19 confirms the value of face-to- face events”:

– 31% (compared to 44% in the previous edition, and 46% in the edition prior to that) believe there will be “Less international ‘physical’ exhibitions and, overall, less participants” (with 4% stating “Yes, for sure”, 27% stating “Most probably” and 26% remaining unsure).

– 61% (compared to 73% and 76% previously) believe there is “A push towards hybrid events, more digital elements at events” (with 19% stating “Yes, for sure”, 42% stating “Most probably” and 20% remaining unsure).

– 6% (compared to 10% and 14% previously) agree that “Virtual events are replacing physical events”, with 16% being unsure and 57% stating “Definitely not”.

The results are similar across regions, with the exception of a significantly higher proportion of companies (35%) being “unsure” that “Virtual events are replacing physical events” in Central and South America.

Background

The 29th Global Barometer survey, concluded in June 2022, provides insights from 366 companies, across 57 countries and regions. It was conducted in collaboration with 19 UFI member associations:

AAXO (The Association of African Exhibition Organisers) and EXSA (Exhibition and Event Association of Southern Africa) in South Africa; AEO (Association of Event Organisers) in the UK; AFE (Spanish Trade Fairs Association) in Spain; AFEP (Asociación de Ferias del Perú) in Peru; AFIDA (Asociación Internacional de Ferias de América) in Central and South America; AKEI (Association of Korean Exhibition Industry) in South Korea; AMPROFEC (Asociación Mexicana de Profesionales en Ferias, Exposiciones, Congresos y Convenciones) in Mexico; AOCA (Asociación Argentina de Organizadores y Proveedores de Exposiciones, Congresos, Eventos y de Burós de Convenciones) in Argentina; IECA/ASPERAPI (Indonesia Exhibition Companies Association) in Indonesia; EEAA (Exhibition & Event Association of Australasia) in Australia; IEIA (Indian Exhibition Industry Association) in India; JEXA (Japan Exhibition Association) in Japan; MFTA (Macau Fair & Trade Association) in Macau; MACEOS (Malaysian Association of Convention and Exhibition Organisers and Suppliers) in Malaysia; SECB (Singapore Exhibition & Convention Bureau) in Singapore; SISO (Society of Independent Show Organizers) in the US; TEA (Thai Exhibition Association) in Thailand; UBRAFE (União Brasileira dos Promotores Feiras) in Brazil.

In line with UFI’s objective to provide vital data and best practices to the entire exhibition industry, the full results can be downloaded at www.ufi.org/research.

The next UFI Global Exhibition Barometer survey will be conducted in December 2022.

Attachments:

– Cover of the 29th edition of the UFI Global Exhibition Barometer report

{kind=link}

– “Regional recovery rates 2022 and H1 2023” infographic

{kind=link}